-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Tianyi Holdings (756.HK) - Profitability maintained stable

Friday, October 16, 2015  13953

13953

China Tianyi Holdings(756)

| Recommendation | Buy |

| Price on Recommendation Date | $0.970 |

| Target Price | $2.000 |

Weekly Special - 3306 JNBY Design Limited

Summary

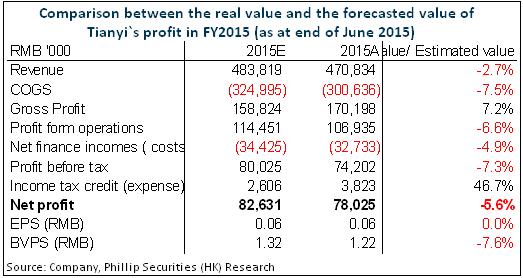

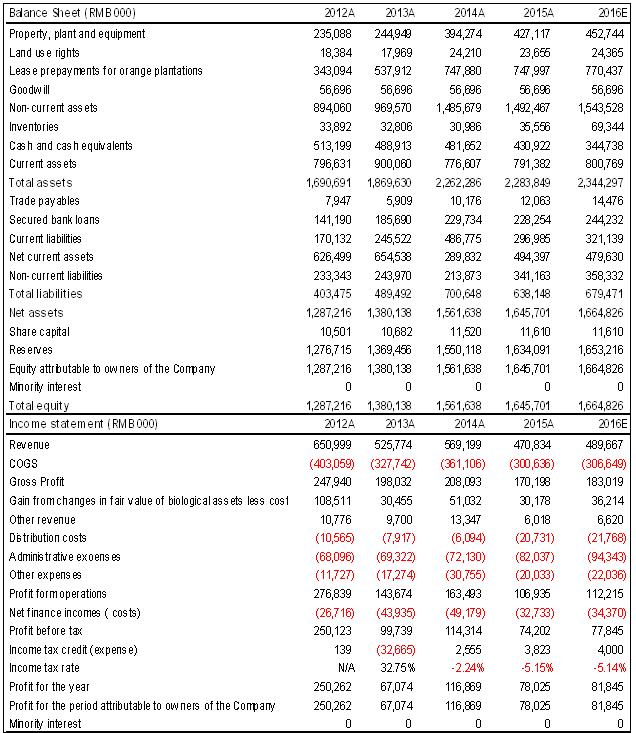

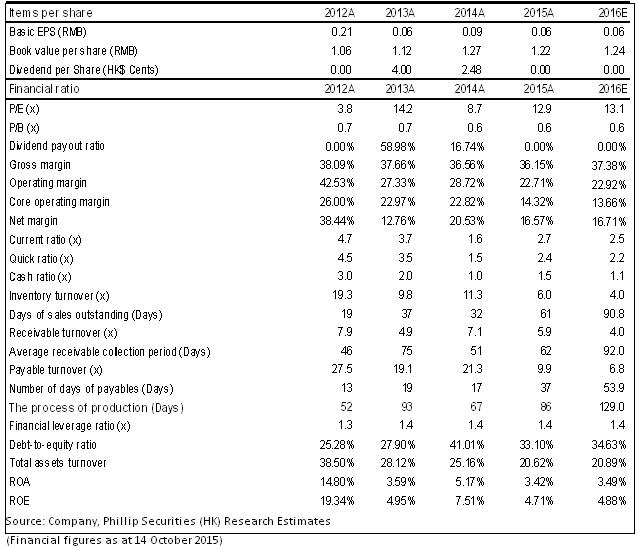

-China Tianyi Holding Limited (“China Tianyi” or “the Group” in the text below) announced its financial report of FY2015, incomes was lower than oue expectation, but the profitability still maintained stable. In June, sale volume of the Group indicated a yoy decline of 17.3% to RMB0.471 billion. Profit attributable to shareholders approximately amounted to RMB78.025 million, down 33.3% yoy, demonstrating a basic EPS around RMB0.06. Even though profit has declined in the period under review, the profitability of the Group can still be maintained stable, with gross profit margin and net profit margin reached 36.1% and 16.70% respectively;

-On the other hand, the Group's financial situation showed obvious improvement, of which financial costs decreased by 33% yoy, with current ratio increased to 2.7 times from 1.6 times recorded in FY2014 (as at end of June 2014) and gearing ratio dropped to 33.10% from 41.0%;

-Cuerrently Tianyi is devoted to business transformation and spends effort on developing Summi as a high-end brand of not-from-concentrated orange juice (NFC 100% juice). The Group also expands inputs on the establishment of e-commerce network. By the end of June, NFC 100% juice's revenue was 2.8% of total revenue. Burst of growth of the business of Tianyi is expected;

-In all, with the positive development prospect of the market, the Group's leading position in the industry and stable profitability, and considering the price decreased obviously recently, we are still very confident on the future performance of Tianyi, and maintain the 12-month target price to HK$2.00, which is 106% higher than the recent closing price, and equivalent to 27.1x of 2016 P/E and 1.3x of 2016 P/B, keeping the rating of “Buy”. (Closing price as at 14 Oct 2015)

Stable profitability

In June, sale volume of the Group indicated a yoy decline of 17.3% to RMB0.471 billion. Profit attributable to shareholders approximately amounted to RMB78.025 million, down 33.3% yoy, demonstrating a basic EPS around RMB0.06. Even though profit has declined in the period under review, the profitability of the Group can still be maintained stable, with gross profit margin and net profit margin reached 36.1% and 16.70% respectively.

Among the current income of Tianyi, the sale of orange juice products still carries the largest share. As at the end of FY2015 (as at end of June 2015), the sale of orange juice products accounted for approximately 62% of the total income. Among this, FCOJ and NFC 100% juice brought an income of approximately RMB280 million and RMB13 million, around 59.5% and 2.8% of the total income respectively. We believe the portion of NFC 100% juice would continue to go up.

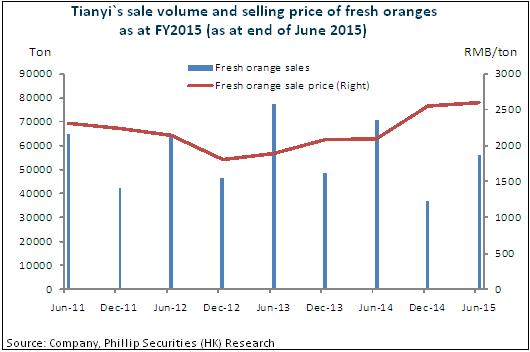

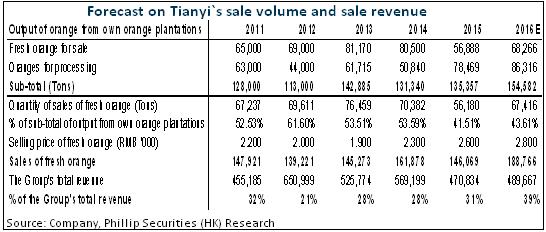

In addition, income contributed from the sale of fresh orange is just behind FCOJ, representing about 31% of the total income, which has increased by 2.6ppts compared to the same period of 2014, amounted to RMB146 million. Such surge is mainly due to the significant increase of the average price of fresh oranges in the period under review: from RMB2,080 per ton in the end of December 2013 increased to RMB2,600 per ton currently. We expect the average price of fresh oranges in the coming few quarters would continue a moderate uptrend. Moreover, considering the fresh orange from approximately70,000 mu (equivalent to 46.67sq km) next year, which means the income contributed from the sale of fresh oranges would keep increasing obviously.

Currenly, the sales trend meets our expectation, and we consider that Tianyi's sale volume in the coming two years would keep steady growth. In a conservative sense, we assume the selling price of fresh oranges would return to the level of approximately RMB2,800 per ton in June 2016, making the Group's fresh oranges sale amounted to RMB189 million, representing 39% of the Group's total income, and the total income would increase in 2016.

Improvement on financial situations

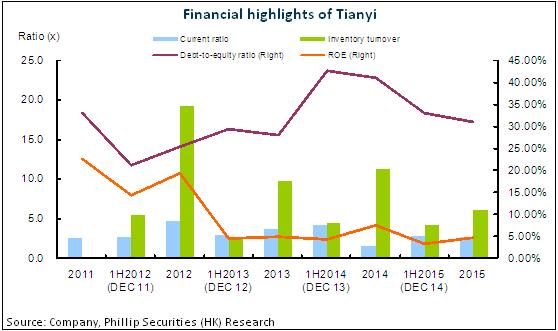

Tianyi still keeps relatively sufficient cash, but the total cash flow declined. As at the end of June 2015, the Group's total cash balance and bank deposit dropped 10.4% compared to the end of 2014. It is worth to note that the Group's accounts receivable surged around 106%. However, owing to the significant decrease of capital expenditure, the Group's financial situation showed obvious improvement, with current ratio increased to 2.7 times from 1.6 times recorded in FY2014 (as at end of June 2014) and gearing ratio dropped to 33.10% from 41.0%.

Risk

High concentration on certain customer segment, sale income highly impacted by market situations;

More intensified market competition, slower-than-expected progress of product promotion;

Short-term decline of share price.

FINANCIALS

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()