-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

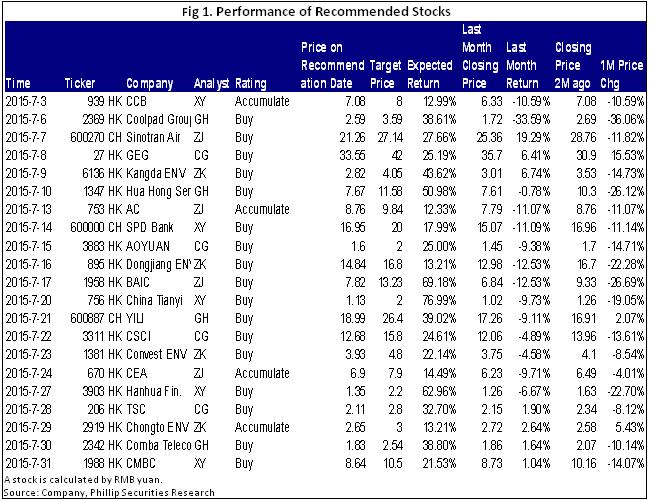

Report Review of July. 2015

Monday, August 3, 2015  13746

13746

Report Review of July. 2015

Weekly Special - 3306 JNBY Design Limited

Sectors:

Mainland financial, Utilities (Xingyu Chen), Mainland Telecom (Fanguohe),Mainland property, Oil and gas service (Chengeng), Air, Automobiles, Infrastructure (ZhangJing), New energy & Environmental Goods (Zhang Kun)

Mainland Financial (Xingyu Chen)

The market continued to go down sharply in July, HSI decreased from 26,300 at the beginning of this month to 24,600 currently, down 6.5% approximately. According to the performance, the banks` share prices still maintained the same trend as the market this month, and most of them declined obviously. Although the banks` interim results will be announced soon, H Shares will be weak continually considering the large market volatility in A Shares recently and it`s quite difficult for the improvement of the banks` performance in the short term.

We expect the banks` operating performance still maintains at the stable level in 1H, and considering the large adjustment recently, the banks` valuation decreases largely, therefore we still hold the cautiously optimistic view on the banks` prices in future. Maintain the banking sector on Buy rating.

Mainland Telecom (Fan guohe)

This month I released 4 equity reports including, Coolpad Group (2369.HK), Hua Hong Semiconductor (1347.HK), YILI (600887.CH) and Comba Telecom (2342.HK). We prefer Coolpad Group with the more attractive future.

LeTV contributed RMB 2.18 billion to hold 18% of Coolpad shares, becoming the second largest shareholder. At the end of 2014, Coolpad announced to form a joint venture with Qihoo 360. The Company`s top priority is to convert itself into an Internet operator. Generally speaking, LeTV will win the mobile phone industry chain and enrich its terminal products from the cooperation, while Qihoo can obtain the access to the Internet traffic. Coolpad`s varied product mixes, 40 million sets of shipment, and 6000 patents provide a basis for the mobile Internet platform. With Qihoo`s security APPs, 360 OS and LeTV`s video contents, the Company is no longer simply a hardware vendor. The three parties are expected to build up a mobile Internet ecosphere consisting of “terminal + APP + platform + contents”. Coolpad`s wireless application services will improve further and are likely to achieve a double growth in the mid-term. Therefore, its profit will come mainly from wireless application services.

Property Industry (Chen Geng)

In July, 2015, I wrote four research reports on Galaxy, Aoyuan, CSCI and TSC, , which got success by unique operation model. We recommend “CSCI”. The endogenous growth of CSCI is resulted from robust increase of new contracts as well as solid and stable operation. The PPP mode of operation and the asset injections from the parent company provided new operation mode, better asset quality and expanded asset scale for the Company. We expect the growth of earnings of CSCI would be kept at the level above 20% in the coming two years, while net debt ratio would be consistently kept at the level lower than 40%. We maintain the rating of “Buy” for CSCI, with the 12-month target price at HK$15.8, which is equivalent to 14.7x and 12.6x of the P/E in 2014 and 2015 respectively.

Automobile & Air (ZhangJing)

This month I released 4 equity reports including, Sinotran Air (600270 CH),BAIC (1598 HK),AC (753 HK) and CEA(670 HK). We prefer Sinotran Air with the more attractive future and the only “cross-border e-commence” stock in A share . The Company has nearly 100 branches and subsidiaries and over 3000 logistics outlets across the country, taking the No.1 position on China`s international air freight forwarding market. To seize the market opportunities, the Company launched China`s first cross-border logistic e-commence platform in 2013, aimed at the emerging logistics market for online overseas purchase. In collaboration with air freight companies by signing a charter agreement, with Tencent by setting up a WeChat platform, with Alibaba`s Tmall and NetEase`s Kaola website, the Company launched a self-operated B2C platform - Sunnytao, in order to quicken innovative business pattern integrating logistics platform, payment platform, transportation channels and delivery network both at home and abroad, laying a solid foundation to explore e-commence finance and logistics. As the only one to carry out clearance cooperation with China Customs, the Company`s prospect is worth expecting with the continuous improvement of network layout and development of cross-border logistic e-commence platform.

New energy & Environmental protection (ZhangKun)

We update four reports this month, they are Kangda ENV (6136.HK), Dongjiang ENV (895.HK), Canvest ENV (1381.HK) and Chongto ENV (2919.HK). We recommend Chongto ENV, The three core business segments of Chongto, namely industrial wastewater treatment, sludge treatment, and hazardous waste treatment, all carry the features of strong profitability and great market potentials. The comprehensive treatment capacity of the Company gives her ability to offer overall integrated solutions to enterprises producing wastewater in industrial park. Diversification of businesses also helps to lower the possible business risk of concentrating on a type of business. Recently, the Company has implemented stock splitting. We raised the target price to HK$3, which is equivalent to 18x of the 2016 eP/E, keeping the rating of “Accumulate”.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()