-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Maple Leaf Education Systems Limited (1317.HK) - Driven by light asset model with a promising outlook of international schools in China

Thursday, July 5, 2018  17846

17846

China Maple Leaf Education Systems Limited(1317)

| Recommendation | Accumulate |

| Price on Recommendation Date | $14.300 |

| Target Price | $15.680 |

Weekly Special - 2333 Great Wall Motor

Investment Summary

China Maple Leaf Education Systems Limited is a leading international school operator, from preschool to grade 12 education (K-12) in China. Thanks to the rise of middle class in China, its light asset development model and unique dual-diploma curriculum, we believe Maple Leaf will be one of the most promising players in the China education sector. We initiate an “accumulate” rating on Maple Leaf, and a target price of HK$15.48 based on earnings in 19F assuming 1x PEG (30% CAGR on earnings for FY18E-20E), with 12.2% potential upside. (Closing price at 3 July 2018)

Corporate Background

Founded in 1995, it is operating 82 schools (where five are new acquisitions, and yet consolidated) in Dalian, Wuhan, Tianjin, Chongqing, Zhenjiang, Luoyang, Shanghai, Shenzhen, etc. The group has accelerated its school expansion in recent years, with 17 net increases in March of 2018, excluding five new acquisitions. Currently, the group comprised of 13 high schools (for students in grade 10 to 12), 21 middle schools (for students in grade 7 to 9), 21 elementary schools (for students in grade 1 to 6), 19 preschools and 3 foreign national schools.

With a total of 29,991 as of March 2018, the number of enrolled students grew at a CAGR of 26% in the past three and half years. As the group aims to establish a pyramid structure of student enrolment from elementary to high schools, the proportion of elementary student students rose from 26% in 2015 to 34% in 2017; whereas that of high school students dropped from 39% in 2015 to 34% in 2017, indicating it is determined to expand its business in compulsory education.

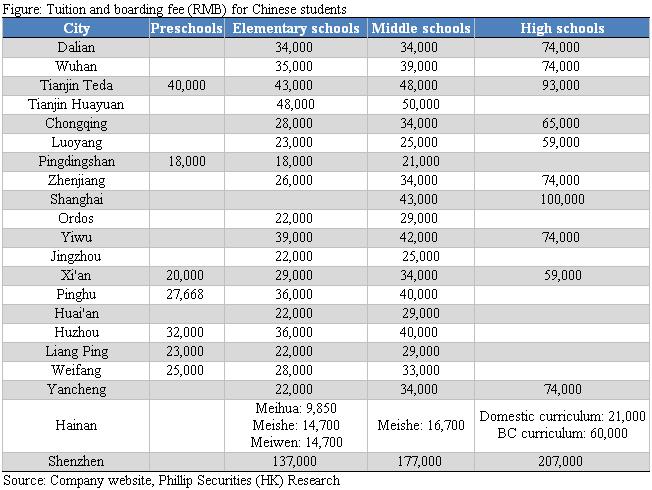

The average tuition and boarding fees for preschools/elementary schools/middle schools/high schools were RMB 29,000/44,850/47,588/86,833 respectively. The average tuition fee per student in 2017 was RMB 38,642 with 2% drop YoY, due mainly to the increase in proportion of elementary school students that charges lower tuition fees than high schools.

Industry overview

The proliferation of middle class in China

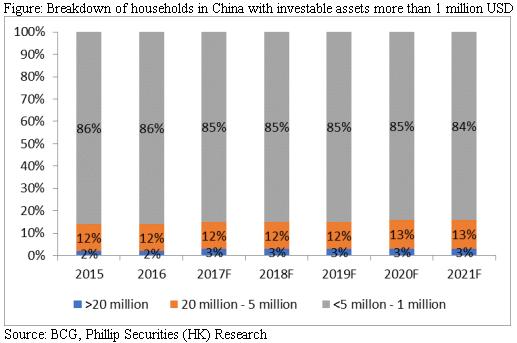

After Chinese economic reform, China has become the world's second largest economy, just behind US. The number of middle class has soared along with the economic development. According to The Boston Consulting Group, the number of households in China with investable assets more than 1 million USD will reach 4 million in 2021, growing in a CAGR of 13.6%. The proportion of households that own more than 5 million USD investable assets also expected to rise from 14% in 2015 to 16% in 2021. The rise in middle class will create a significant demand for international school, as parents are more affordable to the tuition fees.

Steady rise in students studying abroad

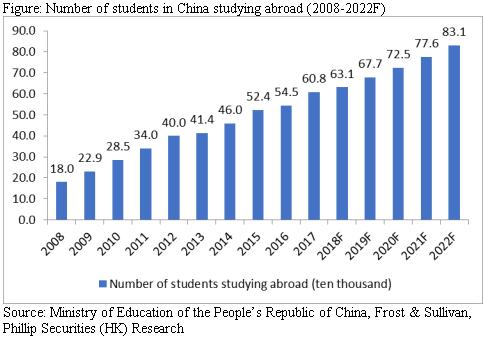

As parents strived to provide better education to their children, studying abroad is gaining popularity in China. According to the Ministry of Education of PRC, the number of students studying abroad increased from 179,800 in 2008 to 608,400 in 2017, growing in a CAGR of 14.5%. Frost & Sullivan predicted the number could reach 830,500 in 2022, with a CAGR of 7.1% during 2018 – 2022. Most of the applications for studying abroad are for undergraduate and postgraduate, which both accounted for 36%. It indicates parents tended to let their children finish K-12 education in China before studying abroad, which will benefit the K-12 international schools that aims to help students prepare for studying abroad, such as Maple Leaf Education.

Limitation on international classes in public school offers opportunities for private international schools

In 2013, Chinese government implemented《高中階段國際項目暫行管理辦法》, in order to limit the supply of international classes in public schools. Municipal government stopped verifying new international classes. The number of international classes dropped by 1 to 224 in 2016; whereas that of private international schools increased by 136 to 392 in 2016. As international classes used to be a substitution for private international schools, the limited supply in international classes will abate intensity of competition in the sector.

Long-term drivers in the future

Light asset development model

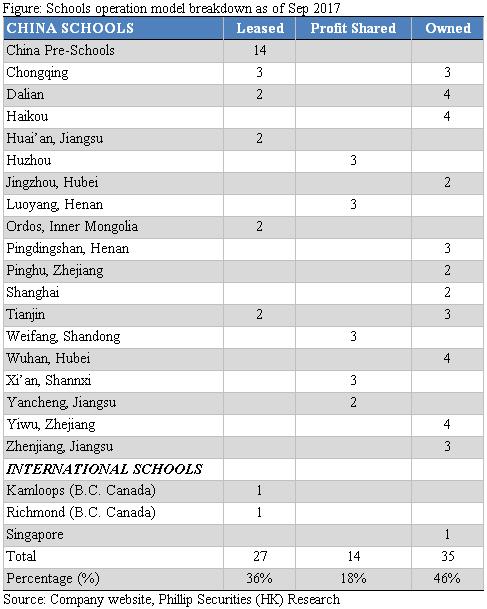

Since 2012, the group started its light asset development model. A light asset development model means the group cooperates with third parties, mainly local government [if the third party is government, then it refers to a Public-private partnership (PPP)], where third parties provides land or school facilities, while the group is responsible for operation, i.e. teacher, teaching material, or facility renovation. The cooperation could be either rental or profit sharing. In rental model, fees are usually determined by number of students or trigger of a certain event. In profit sharing model, the profit is usually shared by half with the third parties.The advantages of light asset development model are 1) shorter payback period and 2) accelerating the expansion.

First, cooperating with third parties, the group could save substantial initial capital expenditure on land and school facilities, which will shorten the payback period from more than two years (self-owned school) to around a year. This model could leverage the group's enriched experience in operations.

Second, with less initial capital expenditure and the help from local government, the group could accelerate its expansion and enlarge its business scale. The larger businesses scale could improve the operating efficiency by sharing the resource across their schools and enhance its reputation, which in turn lead to more PPP projects from local governments.

As of Sep 2017, 54% of its schools are either leased or profit shared. We expect this strategy will continue and the proportion of rental and profit sharing school will be driven up in next few years.

Expansion to top first tier cities

The group first focused on first, second, third and fourth tier cities before expanding to top first tier cities. In the beginning, the group was not as competitive as those renowned schools located in top first cities such as YK Pao School, International school of Beijing, Dulwich College Beijing, etc. However, with more operation experience and reputation accumulated in mid-tier cities, it paves the way for the group to top first tier cities. In 2013, the group set up its first international schools in the top first tier city – Shanghai, and later acquired 55% equity interest in Shenzhen Yisidun Longgang School in 2017, becoming the second schools in the top first city for the group. We expect the group will gradually expand its network in those top first cities by either M&A or self-establishment.

Tuition fee hikes plus increasing source of revenue from additional services

The group confirmed to raise the tuition fees by 25% in Sep 2018 in Dalian, Chongqing, Wuhan, Zhenjiang, Tianjin, and Luoyang. Mgt claimed it is also possible for other schools to raise its tuition fees in Sep, but it is due to confirm. Since the new tuition fees are only subject to new students, we believe the effect in revenue and GPM will take a few years to be reflected. Despite the 25% hike in tuition fees, we believe the group's tuition fees are still competitive compared to other international schools, as the group's tuition fees are much lower than its competitors in the past.

Besides, the group is eager to exploit more sources of revenue by providing additional services, such as overseas studies consulting services, study tour, educational vacation activities, and educational books rental. The revenue from additional services to total revenue ratio increased from 14% in 2013 to 19% in 2017. With more valued-added services provided to students, not only do the students enjoy, the group can also benefit from an extra source of revenue.

Dual-diploma curriculum – PRC and BC high school diploma

The group's high schools are certified by the Ministry of Education of BC, Canada and the Chinese government, where the graduates will be entitled to both a PRC and a BC high school diploma, offering greater flexibility for graduates in the choices.

It takes six steps to be a B.C. certified offshore school, 1) Expression of Interest, 2) Interview, 3) Application, 4) Application Inspection, 5) Pre-Certification, and 6) Certification. First, the applicant contacts ministry staff to request its interest, then the Ministry of Education will review the submission. Second, Ministry of Education representatives will conduct an in-person interview to assess their motivation, capacity to operate an offshore school, and goals and plans for the school. Third, the applicant needs to submit documents, including: Business plan for the offshore school, Audited financial statements, budget forecasts and Local government approvals. Fourth, A Ministry of Education will appoint inspection team performs an on-site inspection of their school. Fifth, if the applicant passes the inspection, they will sign one-year Pre-Certification Agreement with the Ministry of Education. The ministry will decide whether to certify the school based on the recommendations of the inspection team and whether the school meets the requirements set out in the Pre-Certification Agreement. Finally, passing the pre-certification, the applicants then sign one-year Certification Agreement with the Ministry of Education. And, to renew certification, the applicant needs to pass an annual on-site inspection.

We believe the stringent process in B.C. certification will create a barrier to the potential applicants, protecting the advantages of the existing offshore school operators – Maple Leaf Education.

According to BCMOE, 13 out of 38 offshore schools in China are under Maple Leaf Education, accounted for one-third of the total schools.

With BC high school diploma, the graduates could pave their way to top-tier universities, particularly universities in Canada. As BC high school diploma is a diploma certified by Canada, the graduates are easier to admit to universities in Canada than other certifications, such as IB, AP, or A-level. According to the research from JJL Oversea Education, Canada ranked 4th in the most favorite country for Chinese students studying abroad, accounted for 9.51%, just behind United States, United Kingdom, and Australia. We believe the B.C. certified offshore schools of the group will be attractive choices for students targeting to study abroad in Canada.

Excellent record in graduates

Based on Maple Leaf Global Top 100 University Guide compiled by the group (comprises of Top 30 National Universities by US News, Top 10 Liberal Arts Colleges by US News, Top 20 UK Universities by Times Higher Education, Top 10 Medical/Doctoral Universities by Maclean's, Top 10 Comprehensive Universities by Maclean's, Top 10 Australian Universities by QS, and Top 10 SHIN Universities by QS), 56% out of 1,807 graduates received offers from one of the Maple Leaf Global Top 100 universities, and 46 of whom even received offers from top 10 universities in the world, including Imperial College of London and University College of London for the year ended 31 August 2017. The excellent record in graduates reflected the education quality of the group, which will serve as a strong competitive advantage.

Earnings forecast

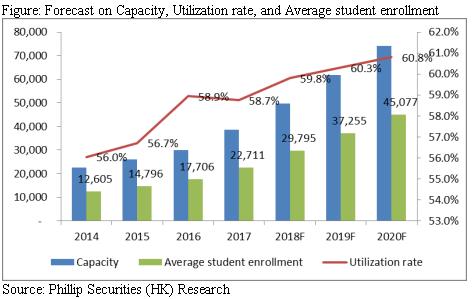

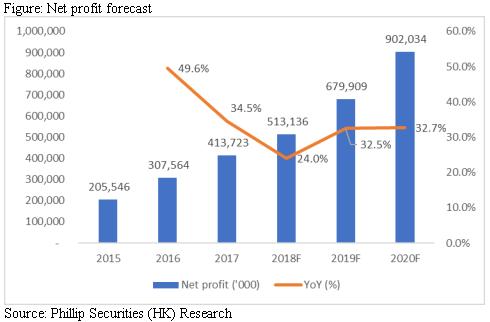

We expect the growth in capacity will remain strong, yet decline in the next three years, with 28.9%/24%/20% for FY18-20E by PPP, M&A, or Self-establishment. Meanwhile, the utilization rate is expected to climb from 58.7 in 2017 to 60.8% in 2020E. We do not have an aggressive estimation on it because of the robust growth in capacity. The average number of students will climb from 22,711 in 2017 to 45,077 in 2020F. Besides, as the group will continues exploring additional services to student, we expect the proportion revenue from additional services will rise from 19% in 2017 to 22% in 2020F. The average tuition fee per students is also expected to hike by 1%/1.5%/2.5% in 2018F-20F in order to reflect the increase in tuition fee starting in Sep 2018. Therefore, we project the growth in revenue will be 34.2%/28.5%/25.6% in 2018F-20F respectively.

As the tuition fee hikes, we expect the GPM will increase from 49.8% in 2017 to 52% in 2020F.

We predict the growth to be 24%/31.1%/28.7% in 2018F-20F, thanks to the increasing GPM, and student enrollments.

Valuation

Thanks to the rise of middle class in China, its light asset development model and unique dual-diploma curriculum, we believe Maple Leaf will be one of the most promising players in the China education sector. Thus, we initiate an “accumulate” rating on Maple Leaf, and a target price of HK$15.68 based on earnings in 19F assuming 1x PEG (30% CAGR on earnings for FY18E-20E), with 9.7% potential upside. (CNY/HKD = 1.17)

Risk

1. VIE structure prohibited in China

2. New acquired schools were not able to add valu

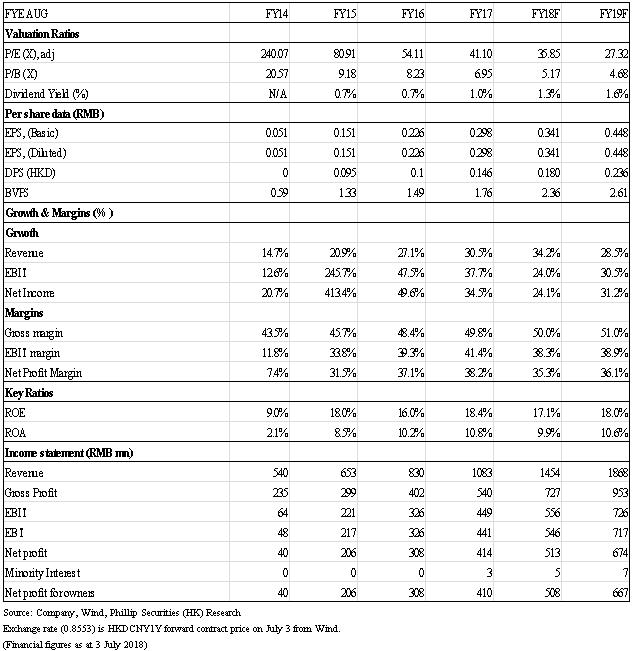

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()