-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CRSC (3969.HK) - Investment in infrastructure projects rebounded in 2019; listing in STI board could be a catalyst

Thursday, June 6, 2019  20223

20223

CRSC(3969)

| Recommendation | Buy |

| Price on Recommendation Date | $5.120 |

| Target Price | $6.640 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

CRSC is a leader in the global rail transportation control system market, which mainly engaged in design and integration, equipment manufacturing and system implementation of rail transportation control systems. It is the only rail transportation control system solution provider in the world, which is capable of independently providing the entire suite of products and services with competitive advantages across the whole industry value chain. We derived a TP of HK$6.64, and upgraded to a “Buy” rating due to the recent drop in share price, with a potential upside of 29.7%.(Closing price at 4 Jun 2019)

Remarkable growth in revenue and external contracts, while GPM dropped

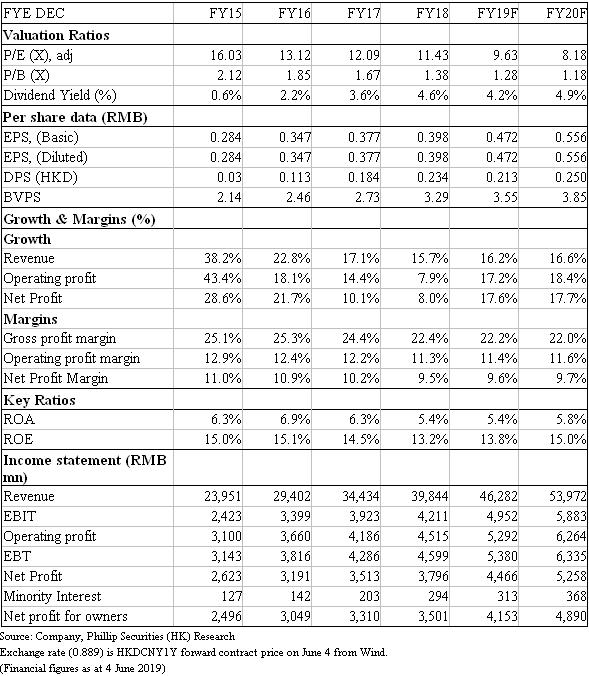

On Mar 20, The Group released its 2018 annual result, which the revenue grew by 15.7% to RMB 39.84 bn, whereas the net profit just rose by 8% to RMB 3.8 bn. During the period, the GPM dropped by 2%, due to the increasing proportion of the business which has a lower GPM; the NPM also reduced by 0.7% to 9.5%. In 2018, the total aggregate amount of external contracts signed by the Group was RMB 68.29 bn, representing an increase of 12.4% over the same period in 2017. The total amount of external contracts signed in Railway, Urban Transit, and Subway were RMB25.08, 11.61 and 11.6 bn respectively. The amount in the General Construction Contracting Business and Other Businesses was RMB 29.85 bn.

Besides, the Group also released the total aggregate amount of external contracts signed for the first quarter. As of 31 Mar 2019, the total aggregate amount of external contracts signed was RMB 7.48 bn, up by 16.1% YoY, in which the amount of external contracts signed in Railway was RMB 3.98 bn, up by 22.5% YoY; the amount in Urban Transit was RMB 1.86 bn, increased by 14.4%; the amount in the Oversea Business was RMB 130 mn, rose sharply by 282.4% YoY; the amount in the General Construction Contracting Business and Other Businesses was RMB 1.52 bn, down by 1.4%

Investment in infrastructure projects rebounded in 2019

Since the government has vigorously promoted de-leveraging in 2018, making local governments difficult to finance, fixed assets investment in transportation, warehousing and postal services has only increased by 4.4% in 2018 and 7.2% YoY in October-December. The Group also indicated that many projects have been suspended. However, as China-US trade conflicts heat up, the uncertainty in China's economic growth rises. At the meeting, the Politburo of the Communist Party of China proposed “Six stables” (Stable employment, Stable finance, Stable foreign trade, Stable foreign investment, Stable investment, Stable expectations).

Among them, "Stable investment" is regarded as an incentive for investment in fixed assets, because in the past when the economic growth slowed down, the investment in fixed assets was used as a countermeasure. In February this year, the National Development and Reform Commission released the National Fixed Assets Investment Development Trend Monitoring Report and the 2019 Investment Situation Outlook", indicating that infrastructure investment is expected to maintain a medium-speed growth in 2019. We believe that infrastructure projects such as transportation will be rebounded in 2019 to offset the impact from foreign trade.

Listing in Science and technology innovation board could become a valuation catalyst

The Group plans to issue A shares on the Science and Technology Board and has been accepted by the Shanghai Stock Exchange. The Group plans to issue no more than 2.197 billion new A shares, and the net proceeds are estimated to be RMB 10.5 bn. It will be used for advanced and intelligent technology research and development projects (including advanced rail transit control systems and key technology research, rail transit intelligent integrated operation and maintenance). System and technology research, smart city and industry communication information system research, etc.), advanced and intelligent manufacturing base projects and supplementary liquidity. As the average valuation of the A-share market is higher than that of the Hong Kong stock market, we expect the Group's valuation in STI Board to be higher than the current Hong Kong market, and could drive up the valuation in Hong Kong market in the future.

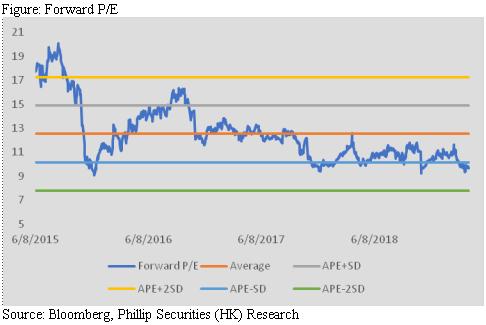

Valuation

Based on a P/E ratio of 12.5x (the average of the past forward P/E), we derived a TP of HK$6.64, implying a P/E of 10.6x in 2020F. Due to the recent drop in share price, we upgraded to a “Buy” rating , with a potential upside of 29.7%. (HKD/CNY=0.889)

Risk

1. Growth of railway investment fails to meet expectations

2. Fierce competition in urban rail market leads to bidding failure

3. Profitability level fails to meet expectations

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()