-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

李浩然先生(Eric Li)

高級分析師

高級分析師

現任現為輝立証券持牌高級分析師,曾任職股票基金、家族辦公室及證券公司等,擁有多年的證券研究部門從業及投資經驗,並先後於香港最暢銷的財經媒體撰寫投資專欄。畢業於香港理工大學電子計算系。

Eric is currently a licensed research analyst at Phillip Securities. Prior to joining Phillip Securities, he has years of equity research and investment experiences in asset management company, family office and securities company. Meanwhile, he has written investment columns in Hong Kong`s best-selling financial media for years. He holds Bachelor of Arts in Computing from The Hong Kong Polytechnic University.

| Phone: | 22776516 | Email: | erichyli@phillip.com.hk | |

ASM Pacific Technology Limited (522.HK) - Might lead to weak sales in 2H 2022

Tuesday, June 7, 2022  2159

2159

ASM Pacific Technology Limited(522)

| Recommendation | Accumulate |

| Price on Recommendation Date | $71.500 |

| Target Price | $85.250 |

Weekly Special - 1773 Tianli International

Better-than-expected 4Q2021 EPS

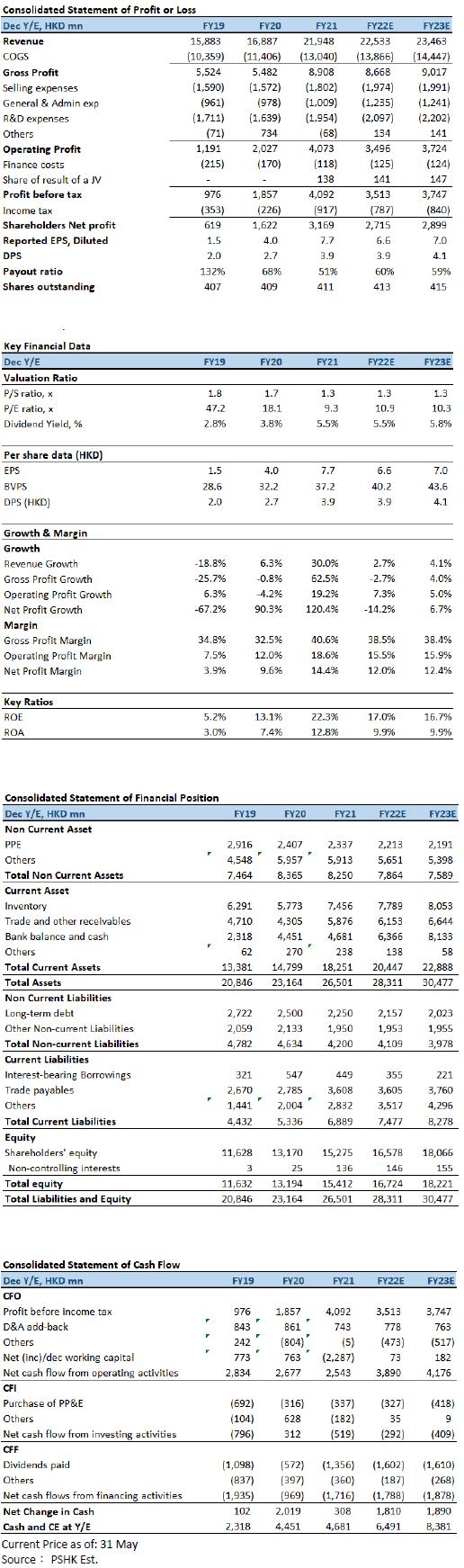

ASMPT delivered revenue of HK$6.20bn (US$796mn) in 4Q2021, increased 43.9% YoY, but dropped 1% QoQ. This exceeded the top end of revenue guidance US$720-770mn issued in the previous quarter’s results announcement and higher than consensus estimates. Bookings of HKD5.25bn (US$674 million), was an increase of 25.0% YoY, but a sequential decline of 8.2%. This dip was largely due to a high base effect and general seasonality trends. Of note, this quarter’s bookings remain elevated compared with prior years’ Q4 levels. The GPM was 41.3%, represented an improvement of 588 bps YoY and 76 bps QoQ, with YoY improvement due largely to relatively stronger gross margin performance across both SEMI and SMT segments. Net Profit attributable to shareholders was HK$913 million, down 8.7% YoY and 9.0% QoQ. ASMPT’s EPS reached HK$2.22, down 8.7% YoY and 8.8% QoQ, but still above consensus estimates.

The revenue of the Semiconductor Solutions Segment in 4Q2021 was HK$4.10bn (US$ 526mn), representing 66.1% of total revenue, up 72.4% YoY and 15.5% QoQ. Bookings of HK$2.79bn (US$358 million), an increase of 7.8% YoY and a decline of 21.4% QoQ. Although this decline is in line with general seasonality trends, it also recorded a decline for the third consecutive quarter. During the same period, revenue from the SMT Solutions Segment reached HK$2.10bn ($270 million), accounting for 33.9% of this quarter’s total revenue, an increase of 8.8% YoY and a decrease of 21.7% QoQ. Bookings of HK$2.46bn (US$316mn), up 52.7% YoY and 13.4% QoQ. The demand momentum from industrial and automotive customers continued into Q4.

In FY2021, the record full year revenue reached a record high of HK$21.95bn (US$2.82bn), an increase of 49.3% YoY, mainly influenced by positive developments in end-markets, including the automotive, consumer and industrial markets expanded significantly with revenue more than doubling YoY, contributing around 16%, 23% and 10% of total revenue; the Communications market experienced strong double digit YoY growth, contributing around 22% of total revenue. This growth was achieved on the back of strong System-in-Package (“SiP”) requirements for smartphone and wearables applications; and computing market, which contributed approximately 12% to total revenue.

1Q2022 Business Highlights

In 1Q2022, ASMPT's revenue was HK$5.27bn (US$675mn), an increase of 21.5% YoY and a decrease of 15.1% QoQ, but still exceeded the median forecast of US$640-690mn issued in the 4Q results announcement. Profit after taxation was HK$830mn, an increase of 57.1% YoY and a decrease of 15.0% QoQ (excluding one-off items amounting to HK$65.5mn in 4Q2021). Basic EPS amounted to HK$2.02, increase of 59.1% YoY and a decrease of 9.0% QoQ. Bookings of HK$7.04bn (US$902.6mn) represented a 10.0% decline YoY due to a record high base effect of Q1 2021, but 34.2% increase QoQ. This sequential growth was mainly driven by AP and automotive bookings momentum. As such, ended the quarter with a strong backlog of HK$11.89bn (US$1.52bn) and a book-to-bill ratio of 1.34 (4Q2021: 0.85). GPM was 40.6%, a 107 bps increase YoY and decline of 69 bps QoQ, notwithstanding cost pressures from key material cost increases (particularly silicon components) and higher logistical costs from a constrained global supply chain environment.

Semiconductor Solutions Segment delivered revenue of HK$2.94bn (US$377.0mn) accounting for 55.9% of quarterly Group revenue. This represented growth of 8.8% YoY and decline of 28.2% QoQ. The IC/Discrete mainstream tools experienced strong YoY revenue growth, hitting a Q1 revenue record. However, the CIS’s revenue declined YoY and was flat QoQ largely due to soft market conditions for smartphones. Segment gross margin was 44.7%, a 68 bps YoY and 103 bps QoQ increase largely due to a favourable product mix, which included a relatively higher proportion of tools serving automotive applications.

SMT Solutions Segment revenue was a robust HK$2.32bn (US$297.8mn), accounting for 44.1% of Group revenue. This represented strong growth of 42.4% YoY and 10.5% QoQ. This sequential growth bucked typical revenue trends. Both mainstream high-end printing and placement tools grew YoY and QoQ, while the Segment’s AP tools - particularly SiP placement tools - delivered YoY growth. Segment gross margin was 35.5%, representing 331 bps growth YoY but 125 bps decline QoQ. The YoY improvement was mainly due to relatively higher volume effect and favourable product mix, segment profit had a 165.1% YoY and 34.4% QoQ increase.

Company valuation

The company expects 2Q2022 revenue to be between US$670-740mn, representing growth of 5.8% YoY and 4.5% QoQ at mid-point. While bookings for the Advanced Packaging (AP) tools hit a record this quarter, including USD100mn of TCB bookings for its major customer (likely from Intel); Bookings for the advanced packaging and automotive solutions growth for both QoQ and YoY, remains a long-term capability requirements driver. However, sporadic COVID-19 measures and continued supply chain constraints could not convert its strong order backlog at a faster pace and influence near-term deliveries. In addition, ASMPT expects bookings to decline QoQ and YoY in 2Q22, as some OSAT vendors reduce capex for legacy, packaging after an aggressive expansion cycle in 2020-2021, consequently, which might lead to weak sales in 2H2022. Recently, ASMPT was removed from the Hang Seng Technology Index, but its component weight in the index is only 1.79%. Therefore, the selling pressure of passive funds is quite limited, and the impact will only appear in a short period of time. We expect 2022 estimated EPS to be HK$6.6, and our target price is HK$85.25 (13x 2022 P/E, in line with its 5 years average minus one standard deviation), with an " Accumulate " rating.

Risk factors

1) The semiconductor industry has entered a downward cycle; 2) The penetration rate of new products is lower than expected; and 3) The demand for downstream upgrades is lower than expected.

* The analyst has a financial interest in the listed corporation covered in this report.

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()