-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

BJ ENT WATER(371.HK) Leading Enterprise in Water Industry, “Dual Platform” Boost Light Assets Transformation

Thursday, July 11, 2019  8921

8921

BJ ENT WATER(371)

| Recommendation | BUY |

| Price on Recommendation Date | $4.740 |

| Target Price | $5.810 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Leading enterprise in water industry, the main businesses grow steadily

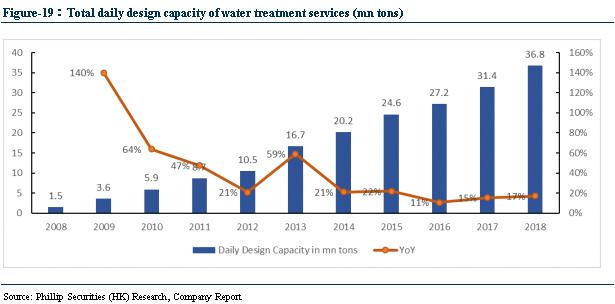

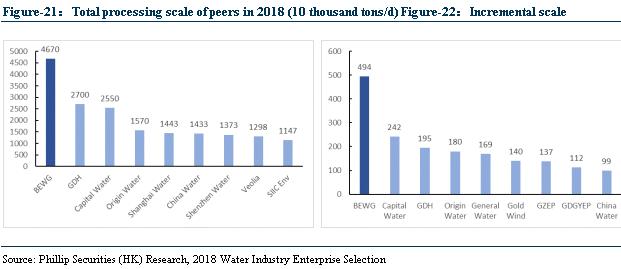

The principal businesses of the Company include operations in water treatment business, construction and technical services for the water environmental renovation. The coverage of the Company's water plants has extended to 21 provinces, 5 autonomous regions and 2 municipalities all across Mainland China. As at 31 December 2018, the Company entered into service concession arrangements and entrustment agreements for a total of 937 water plants including 771 sewage treatment plants, 139 water distribution plants, 25 reclaimed water treatment plants and 2 seawater desalination plants. Total daily design capacity for new projects secured for the year was 5,756,813 tons, total daily design capacity was 36,824,633 tons. Since 2018, the CAGR of total daily design capacity is 37.71%. 17th Water Industry Strategy Forum released 2018 annual water industry enterprises selection list, the Company ranked No.1 among top ten influential enterprises in the water industry in 2018 with 46.7mn tons/day of total water processing scale and 4.94 tons/day of total incremental processing scale

“Dual Platform” Strategy Boosts Light Assets Transformation

The company has determined the strategic direction of light assets transformation, and gradually turned itself into a light asset enterprise by building an asset management platform and an operation management platform - “dual platform”. The company's asset management platform is to co-operate with third-party institutions to establish a fund management company - Beijing Enterprises Jinfu (Beijing) Investment Shareholding Co., Ltd. to provide financial supports for the company's projects. In terms of operation management platform, through the establishment of “Digital Research Institute”, the company built up an intelligence water platform and a procurement center to improve operational management efficiency, reduce manpower and operating costs, and achieve value growth. It's expected that the company's "dual platform" strategy will continue to promote each other, and the company's ability to transform from heavy assets to light assets will continue to strengthen.

Cooperation with China Three Gorges Corporation, Promising on “Yangtze River Protection”

China Yangtze Power Co., Ltd., a controlling subsidiary of China Three Gorges Corporation, subscribed for a 5% stake in BEWG through a wholly-owned subsidiary China Yangtze Power International (HK) Co., Ltd. In January 2019, the Ministry of Ecology and Environment and the National Development and Reform Commission jointly issued the "Action Plan for the Protection and Rehabilitation of the Yangtze River". In June 2019, the newly established joint venture company by BEWG, China Three Gorges Corporation and other companies was awarded the first PPP project in Yueyang City with a total investment of RMB 4.45 billion. The Company believes that the “Yangtze River Protection” is expected to have a market value of more than one trillion RMB, and with the company's rich experience in water treatment projects, operational advantages and sufficient technology precipitation, it can cooperate well with China Three Gorges Corporation to achieve a significant synergy effect.

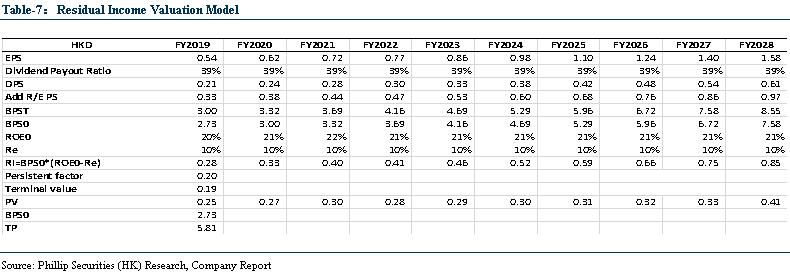

Initial coverage with TP of HKD 5.81 and investment rating of “BUY”

Based on our residual income valuation model, we initiate coverage on BJ Ent Water with a TP of HKD 5.81, corresponding to FY19/FY20/FY21 10.71x/9.36x/8.04x PER with a 22.57% potential upside compared with CP of HKD 4.74 as of July 8, 2019, and recommend “BUY” investment rating.

Industry Analysis

The current status of water quality in China

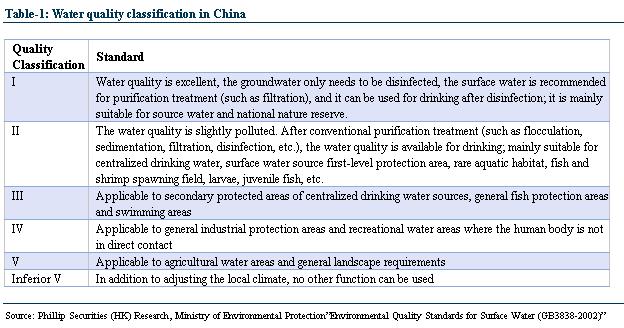

According to the “Environmental Quality Standards for Surface Water (GB3838-2002)” issued by Ministry of Environmental Protection, the water quality in China is divided into six grades: I, II, III, IV, V and inferior V, of which I-III is good water quality.

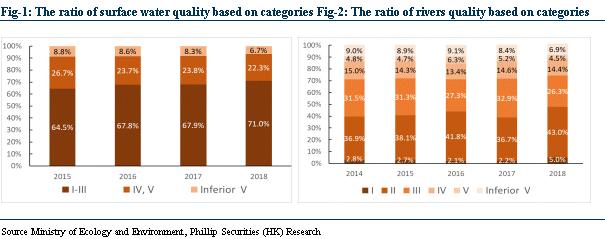

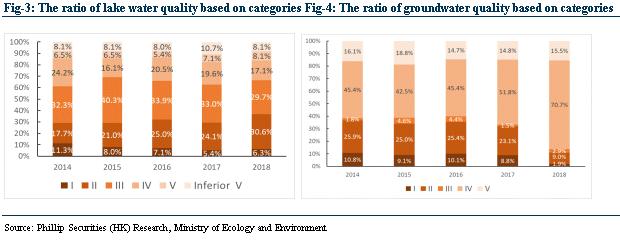

According to the China Ecological Environment Bulletin" issued by the Ministry of Environmental Protection, the water quality of surface water and rivers in China has gradually improved in 2018, but the water quality of lake water and groundwater is not optimistic. The current status of water quality is shown as follows based on the classification:

- For surface water, the proportion of I~III was 74.3%, up 3.1% YoY; the proportion of inferior V was 6.9%, down 1.6% YoY.

- For rivers, the proportion of Class I was 5.0%, up 2.8% YoY; the proportion of Class II was 43.0%, up 6.3% YoY; the proportion of Class III was 26.3%, down 6.6% YoY; the proportion of Class IV was 14.4%, down 0.2% YoY. The proportion of V is 4.5%, down 0.7% YoY; the proportion of inferior V is 6.9%, down 1.5% YoY.

- Among the 111 important lakes (reservoirs), there are 7 lakes (reservoirs) with Class I water quality, accounting for 6.3%, up 0.9% YoY; 34 of Class II, accounting for 30.6%, up 6.5% YoY; 33 of Class III, accounting for 29.7%, down 3.3% YoY; 19 of Class IV, accounting for 17.1%, down 2.5% YoY; 9 of both Class V and inferior V, accounting for 8.1%, up 1% YoY and down 2.6% YoY, respectively. The main pollution indicators are total phosphorus, chemical oxygen demand and permanganate index.

- Among the 10,168 national groundwater quality monitoring points in China, Class I water quality monitoring points accounted for 1.9%, down 6.9% YoY; Class II accounted for 9.0%, down 14.1% YoY; Class III accounted for 2.9%, up 1.4% YoY; Class IV Accounted for 70.7%, an increase of 18.9% YoY; Class V accounted for 15.5%, an increase of 0.7% YoY. The over-standard indicators are manganese, iron, turbidity, total hardness, total dissolved solids, iodide, chloride, "tri-nitrogen" (nitrite nitrogen, nitrate nitrogen and ammonia nitrogen) and sulfate.

The current status of water industry in China

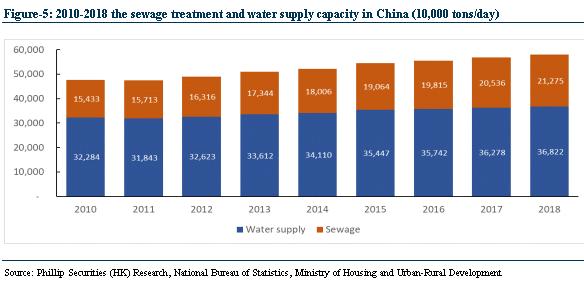

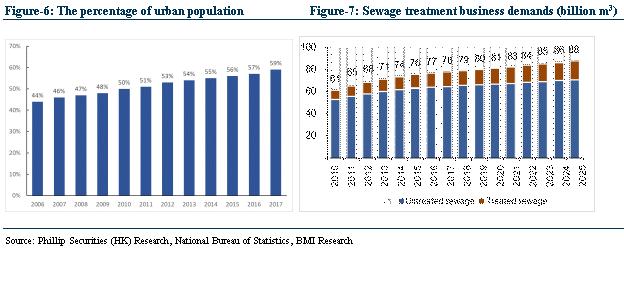

The growth of urbanization in China has created long-term demand for water and sewage treatment business. By the end of 2016, China had built 3,552 sewage treatment plants in urban and rural cities, with the sewage treatment capacity of about 190 million m3/day, and the growth rate was between 4%-6% in recent years. In terms of water supply, by the end of 2016, the urban water penetration rate has reached 98.4%, and the county water penetration rate has also reached 90.5%. In recent years, the construction of water supply facilities has approached saturation, and the total urban water supply in China has remained basically stable, maintaining a growth rate of 1%-3%.

According to the statistics from National Bureau of Statistics, the proportion of urban population in China was 59% in 2017, and it showed an increasing trend year by year. Correspondingly, according to BMI Research, the sewage treatment demand in China will reach 88 billion m3 by 2025. The sewage treatment market in China has strong demand and insufficient supply, and there are many long-term opportunities in the future sewage treatment business.

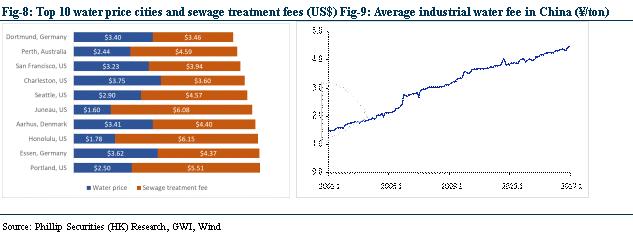

According to the 2017 Global Water Price White Paper released by GWI, water price in China is much lower than that of other countries in the world. The highest water price in China is less than one tenth of the most expensive city in the world, and sewage treatment fees are also much lower than that of the top ten cities with the most expensive water prices in the world. There is still much space for improvement in the water price and sewage treatment fees in China.

Policy promotion, water environment treatment market still has huge room for development

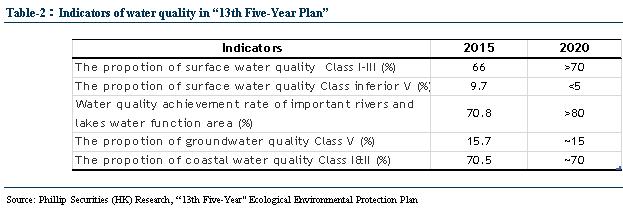

According to the “13th Five-Year Plan for Ecological Environmental Protection” issued by the State Council in November 2016, by 2020 the proportion of the water quality of centralized drinking water sources at or above the prefecture level reaching or exceeding Class III will be more than 93%; the trend of increasing pollution will be initially curbed, the proportion of groundwater with extremely poor quality is controlled at around 15%; the proportion of black and odorous water in urban built-up areas is controlled within 10%, and other cities strive to eliminate heavy black and odorous water bodies; rivers near coastal provinces (districts, cities) into the sea basically eliminate the inferior V water; all county towns and key towns have sewage collection and treatment capacities, urban and county sewage treatment rates reach 95% and 85%, respectively; prefectural and above cities basically realize the complete collection and treatment of sewage; improving the level of sewage recycling and sludge disposal, vigorously promote sludge stabilization, harmlessness and resource treatment and disposal, and achieves harmless treatment and disposal rate of municipal sludge at prefecture level at 90%, the Beijing-Tianjin-Hebei region reach 95%; the utilization rate of reclaimed water in the water-deficient city reaches more than 20%, and the Beijing-Tianjin-Hebei region reaches more than 30%; promote the construction of sponge city, which can reach the area of utilizing 70% of the rain more than 20% of the total area, and the water-deficient cities of the prefecture level and above all meet the national water-saving city standard requirements, Beijing-Tianjin-Hebei, the Yangtze River Delta and Pearl River Delta regions should complete one year ahead of schedule. The “13th Five-Year Plan” of ecological environmental protection water environment quality mainly includes the following indicators:

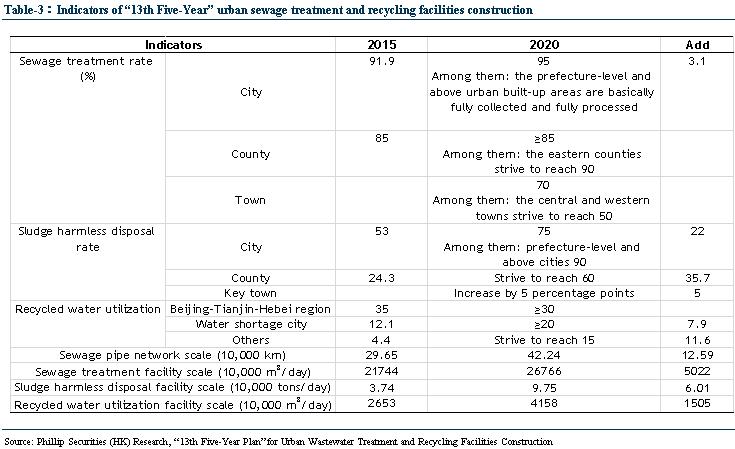

According to the “13th Five-Year Plan for Urban Wastewater Treatment and Recycling Facilities Construction” jointly prepared by the National Development and Reform Commission and the Ministry of Housing and Urban-Rural Development in December 2016, as of 2015, the national urban sewage treatment capacity has reached 217 million cubic meters/day, the urban sewage treatment rate reached 92%, and the county sewage treatment rate reached 85%. During the “13th Five-Year Plan” period, the newly added sewage pipe network was 125,900 kilometers, including 66,200 kilometers of city and 29,200 kilometers of county and 30,500 kilometers of town; the old sewage pipe network transformation is 27,700 kilometers, including 15,800 kilometers of city, 0.73 million kilometers of county, 0.46 million kilometers of town; 28,800 kilometers of merged pipe network, 17,000 kilometers of city, 11,700 kilometers of county seat. The newly-added sewage treatment facilities have a scale of 50.22 million cubic meters per day, of which the city has a scale of 28.56 million cubic meters per day, the county has 10.71 million cubic meters per day, and the town has 10.95 million cubic meters per day. the scale of the sewage treatment facilities was upgraded to 42.2 million cubic meters per day, including 36.39 million cubic meters per day in the city and 5.81 million cubic meters per day in the county; new sludge (water-containing 80% wet sludge) has a harmless disposal scale of 60,100 tons/day, including 45,600 tons/day for the city, 9,200 tons/day for the county, and 5,300 tons/day for the town; The newly-added reclaimed water utilization facility has a scale of 15.05 million cubic meters per day, of which 12.14 million cubic meters per day of the city and 2.91 million cubic meters per day of the county.

In terms of investment, the “13th Five-Year” urban sewage treatment and recycling facilities construction has invested a total of about RMB 564.4 billion. Among them, the investment in various types of facilities construction was RMB 560 billion, and the investment in supervision capacity building was RMB 4.4 billion. In the construction investment, the newly-built supporting sewage pipe network was invested RMB 213.4 billion, the old sewage pipe network transformation investment was RMB 49.4 billion, the rain-sewage pipe network transformation investment was RMB 50.1 billion, and the newly added sewage treatment facility investment was RMB 150.6 billion. The investment in sewage treatment facilities was RMB 43.2 billion, and the investment in new or modified sludge treatment and disposal facilities was RMB 29.4 billion, and the investment in newly added reclaimed water production facilities was RMB 15.8 billion. During the “13th Five-Year Plan” period, the investment in construction of cleaning the black and odorous water body at the prefecture level and above was about 170 billion yuan, which has been included in the planned key construction task investment.

The water industry is less concentrated and the market capacity is still expanding

According to research by the Qianzhan Industrial Research, there are more than 4,000 waterworks in China, more than 3,500 sewage treatment plants, and many water companies. However, the industry concentration is quite low: the operating scale market share of CR5 is 11%, and CR10 is 16.5%, and the market concentration in the water distribution is relatively low. In the sewage treatment industry, the market share of CR5 wastewater treatment enterprises is 19%, and the market share of CR10 is 27.2%. Compared with the water distribution market, the concentration of the sewage treatment market is relatively high. Excessive market fragmentation restricts the technological progress of the water industry and the intensification of services. It is expected that the industry leaders will carry out more mergers and acquisitions in the future, break the technical and geographical restrictions and form a competitive landscape dominated by several major water groups through the expansion.

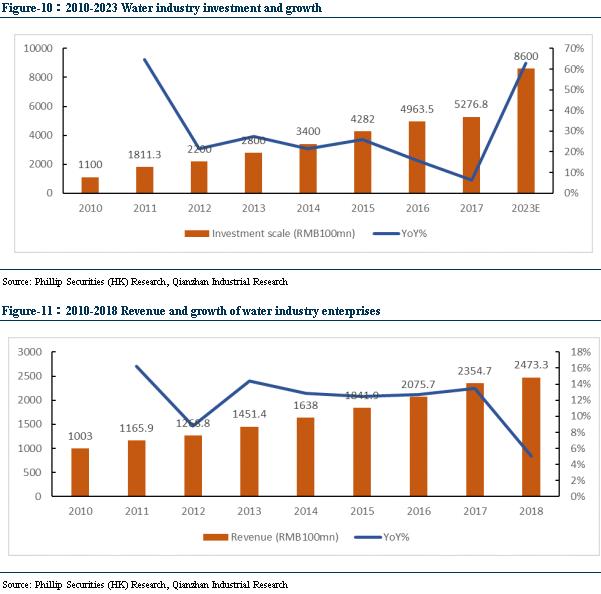

As a weak cyclical industry, the water industry is highly correlated with factors such as economic growth level, population size and urbanization process. In recent years, the regulatory requirements for industry have been continuously strengthened, and the fields of black-odorous water treatment, construction of sponge cities, and township sewage treatment have grown rapidly. Overall, the scale of investment in the water industry has continued to increase, and there still have space for development in market capacity. According to Qianzhan Industrial Research, the annual growth rate of investment in the water industry during the “Twelfth Five-Year Plan” period was 24%. It is estimated that by 2023, the annual investment amount of water industry in China will exceed RMB860 billion.

Company Analysis

Company Profile

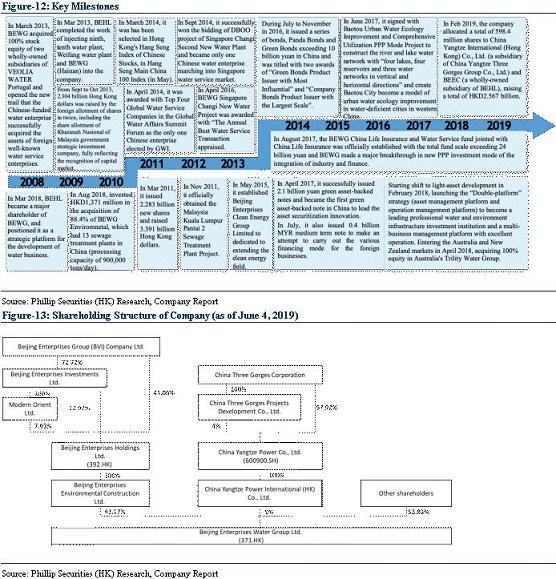

The company which is listed on the Main Board of The Stock Exchange of Hong Kong Limited (Stock Code: 0371), is a large-scale group which provides a broad range of water services and environmental protection services in China. In 2008, Beijing Enterprises Holdings Limited (BEHL) acquired Shanghua Holdings Co., Ltd. and renamed it as Beijing Enterprises Water Group Ltd. (BEWG) and positioned it as the listing platform for Beijing Enterprises Water Business. The company has two main businesses, namely the water treatment services and construction services for the water environmental renovation. In terms of water treatment services, there are currently more than 900 water plants in the world, covering various water plant types, with a total contracted design capacity of 36.82 million tons/day. In terms of construction services for the water environmental renovation, the total signed contract of projects was more than RMB40.4 billion.

Currently, the company has owned and operated over hundreds of water supply plants and sewage treatment plants in China, Malaysia, and Portugal, with daily design water treatment capacity over thirty million tons per day. This represents the company has successfully accomplished its nationwide strategic layout and established a strong presence in the oversea market. Throughout the years, the company was consistently awarded "China Water Service Outstanding New Enterprises", "Best Water Business Enterprises in China", and consecutively ranked No.1 "Top 10 influential Enterprises in the Water Industry" in 2010-2013. The company is the flagship of BEHL (Stock Code: 0392) in the water service market. BEHL has been listed on the main board of The Stock Exchange of Hong Kong Limited since May 1997. Backed by the People's Government of Beijing Municipal, BEHL focuses its core businesses on urban natural gas distribution and infrastructure facilities. BEHL, a diversified utility conglomerate, spots a red-chip status in The Stock Exchange of Hong Kong Limited and is ranked No.1 in "Top 500 Public Utilities and Facilities Enterprises in China".

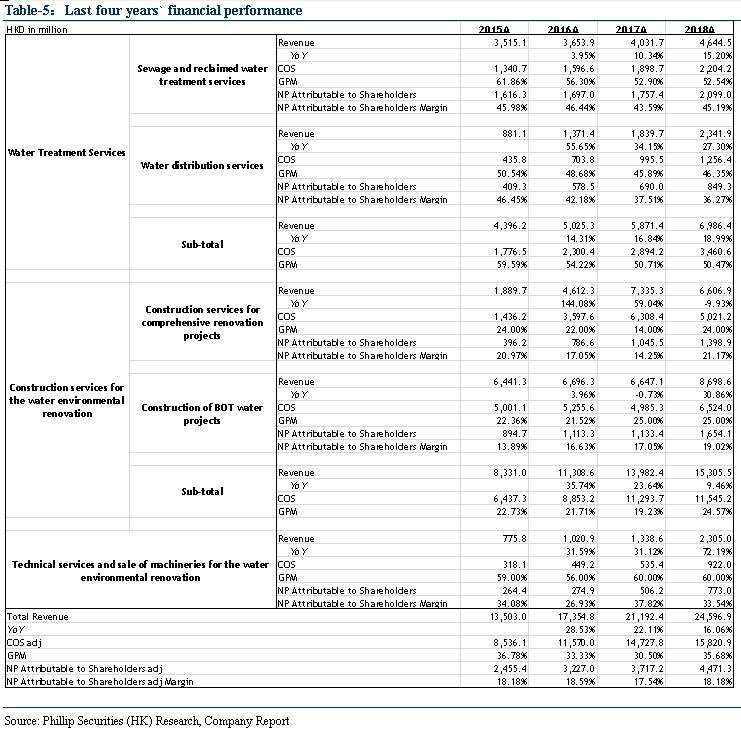

In 2018, the revenue of the company was HKD24.60 billion, with a YoY increase of 16%; net profit contributed to owners was HKD4.47 billion, an increase of 20% YoY. As of Dec 31, 2018, the new net processing scale of the company was 5.44 million tons/day, and the total design capacity was 36.82 million tons/day.

Key Business Analysis

The company is a flagship enterprise devoted to the recycling of water resources and the protection of water ecology subordinated to BEHL, the biggest urban investment, construction and operation service provider in China ranking 198 among China's top 500 enterprises. The company is a comprehensive and leading professional water and environment service provider with its business covering industrial investment, design, construction, operation, technical services and capital operation in full industrial chain. It ranks first in the industry in China in terms of total assets, total revenues and water treatment capacity. The main businesses of the company are water treatment services, construction services, technical services and sale of machineries for the water environmental renovation. Among them, water treatment services are including sewage and reclaimed water treatment services and water distribution services, construction services for the water environmental renovation are including comprehensive renovation projects and construction of BOT water projects.

1.Water treatment services

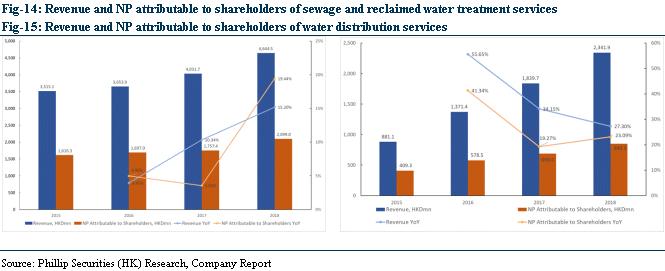

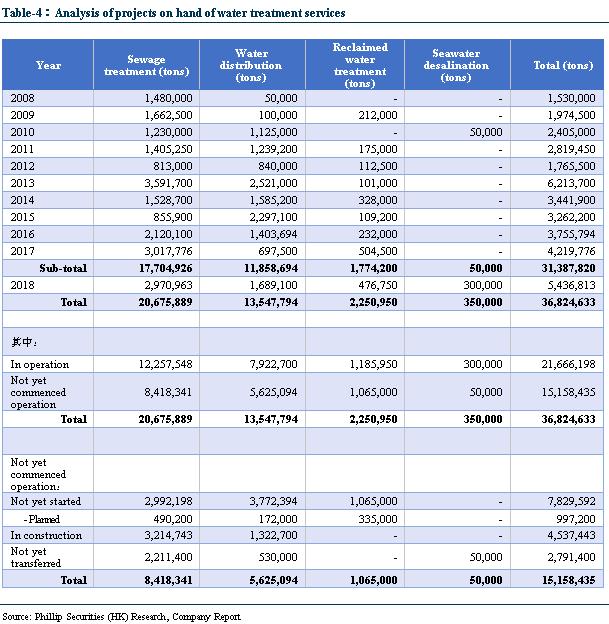

As at 31 December 2018, the company had 274 sewage treatment plants and 10 reclaimed water plants in operation in Mainland China. Total daily design capacity in operation of sewage treatment plants and reclaimed water plants reached to 12,031,550 tons (2017: 11,059,750 tons) and 809,200 tons (2017: 617,200 tons) respectively. The average daily processing volume is 10,704,386 tons and average daily treatment rate is 87%. The actual average contracted tariff charge of water treatment was approximately RMB1.10 per ton (2017: RMB1.08 per ton) for water plants. The actual aggregate processing volume for the year was 3,799.8 million tons, of which 3,493.2 million tons was contributed by subsidiaries and 306.6 million tons was contributed by joint ventures. Total revenue for the year was HKD4,276.1 million. Net profit attributable to shareholders of the Company was HKD2,040.3 million, of which HKD1,894.0 million was contributed by subsidiaries and HKD146.3 million was contributed by joint ventures and associates. The company had 37 sewage treatment plants and 4 reclaimed water plants in Portugal, Macau, Singapore, Australia and New Zealand. Total daily design sewage treatment capacity in operation was 602,748 tons. The actual processing volume for the year is 160.1 million tons. Total revenue for the year was HKD368.4 million. Profit attributable to shareholders of the Company was HKD58.7 million.

For water distribution services, the company had 77 water distribution plants in operation as of 31 December 2018. Total daily design capacity in operationwas 6,715,600 tons (2017: 6,555,600 tons). The actual average contracted tariff charge of water distribution is approximately RMB2.07 per ton (2017: RMB2.14 per ton). The aggregate actual processing volume is 1,441.5 milliontons, of which 794.2 million tons was contributed by subsidiaries, which recorded revenue of HKD1,839.3 million and 647.3 million tons was contributed by joint ventures. Imputed interest income of HKD25.5 million was recognized for the receivables under service concession arrangement of Plant No. 9 in Beijing. Profit attributable to shareholders of the Company was HKD723.5 million, of which profit of HKD590.7 million was contributed by subsidiaries and a profit of HKD132.8 million in aggregate was contributed by joint ventures. The company had 33 water distribution plants and a sea desalination plant which supplies drinking water in Portugal and Australia. Total daily design capacity in operation was 1,507,100 tons. The actual processing volume for the year is 103.5 million tons of which 69.8 million tons was contributed by subsidiaries and 33.7 million tons was contributed by joint ventures. Total revenue for the year was HKD502.6 million. Profit attributable to shareholders of the company was HKD125.8 million.

2.Construction services for the water environmental renovation

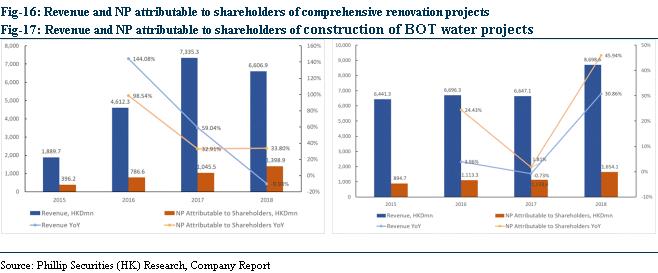

The company had 23 comprehensive renovation projects under construction during the year. Revenue from comprehensive renovation projects decreased by HKD728.4 million from last year of HKD7,335.3 million to HKD6,606.9 million this year. Revenue decreased was mainly due to the decrease in contribution work for Inner Mongolia during the year. Interest income from water environmental renovation projects attributable to shareholders of the company was HKD105.9 million for this year (2017: HKD52.6 million). Profit attributable to shareholders of the company for the comprehensive renovation projects increased by HKD353.4 million from last year of HKD1,045.5 million to HKD1,398.9 million this year.

The company entered into a number of service concession contracts on a BOT basis in respect of its water treatment business. In 2018, water plants under construction were mainly located in Shanxi, Shandong, Zhejiang, Guizhou, Hunan and Hebei provinces. Total revenue for construction of BOT water projects was HKD8,698.6 million (2017: HKD6,647.1 million) and profit attributable to shareholders of the company was HKD1,654.1 million (2017: HKD1,133.4 million).

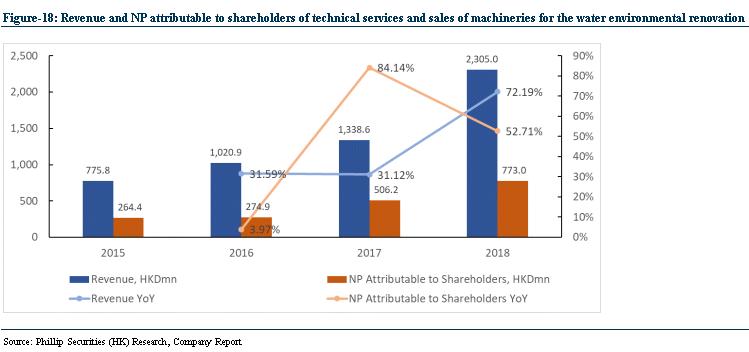

3. Technical services and sales of machineries for the water environmental renovation

The Group has couples of qualifications in engineering for consulting and design of water treatment plants. Revenue from the provision of technical services and sales of machineries was HKD2,305.0 million (2017: HKD1,338.6 million), representing 9% of the company's total revenue. Profit attributable to shareholders of the company was HKD773.0 million (2017: HKD506.2 million).

Investing Highlights

Leading enterprise in water industry, the main businesses grow steadily

The principal businesses of the Company include operations in water treatment business, construction and technical services for the water environmental renovation. The coverage of the Company's water plants has extended to 21 provinces, 5 autonomous regions and 2 municipalities all across Mainland China. As at 31 December 2018, the Company entered into service concession arrangements and entrustment agreements for a total of 937 water plants including 771 sewage treatment plants, 139 water distribution plants, 25 reclaimed water treatment plants and 2 seawater desalination plants. Total daily design capacity for new projects secured for the year was 5,756,813 tons including Build-Operate-Transfer (“BOT”) projects of 320,000 tons, Transfer-Operate-Transfer (“TOT”) projects of 175,000 tons, Public-Private Partnership (“PPP”) projects of 1,824,250 tons, entrustment operation projects of 958,656 tons, and 2,478,907 tons through mergers and acquisitions.

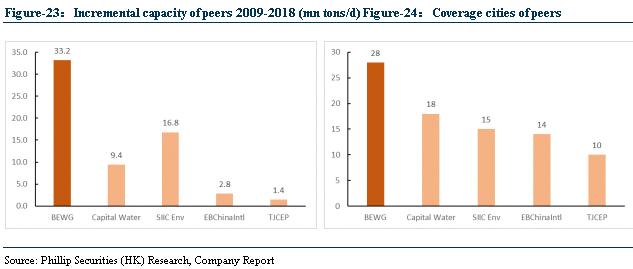

Due to different reasons such as expiration of projects, the Group exited projects with aggregate daily design capacity of 320,000 tons during the year. As such, the net increase in daily design capacity of the year was 5,436,813 tons. As at 31 December 2018, total daily design capacity was 36,824,633 tons. Since 2018, the CAGR of total daily design capacity is 37.71%.

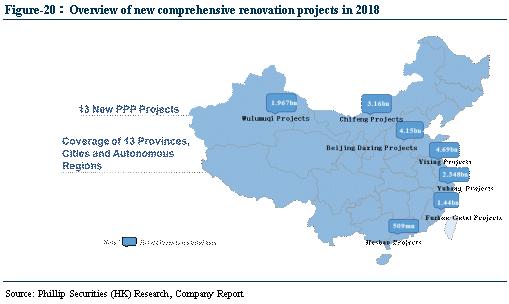

The Company had 23 comprehensive renovation projects under construction during the year. The projects mainly located in Zhejiang Hangzhou, Zhejiang Taizhou, Chengdu Jianyang, Guangdong Heshan, Malaysia Terengganu, Inner Mongolia, Sichuan Luzhou and Beijing Liangshuihe.

The company's water treatment scale and incremental capacity are leading the industry, with the largest water treatment capacity among Hong Kong-listed water companies. In addition, the coverage of company's projects is also the largest, a large number of high-quality projects throughout the country forms a national scale advantage. On March 23, 2019, 17th Water Industry Strategy Forum released 2018 annual water industry enterprises selection list, the Company ranked No.1 among top ten influential enterprises in the water industry in 2018 with 46.7mn tons/day of total water processing scale and 4.94 tons/day of total incremental processing scale.

“Dual Platform” Strategy Boosts Light Assets Transformation

In order to better cope with the new situation and challenges of the environmental protection industry, the company has determined the strategic direction of light assets transformation, and gradually turned itself into a light asset enterprise by building an asset management platform and an operation management platform - “dual platform”. The company's asset management platform is to co-operate with third-party institutions to establish a fund management company - Beijing Enterprises Jinfu (Beijing) Investment Shareholding Co., Ltd. to provide financial supports for the company's projects through fund operations such as fund holdings and asset securitization for water environmental assets to address financing pressures and promote industrial development with new financial means. There are two wholly-owned shareholding platforms under Beijing Enterprises Jinfu: Beijing Enterprises South-South (Tianjin) Investment Management Co., Ltd. and Beijing Enterprises Hengshi (Tianjin) Investment Management Co., Ltd. The former one is the asset management platform of BEWG, and mainly provides organization, management and operation service for industrial funds related to PPP projects of BEWG. The latter one is the investment platform of BEWG and mainly takes part in the investment of the related PPP industrial funds of BEWG.

In terms of operation management platform, through the establishment of “Digital Research Institute”, the company built up an intelligence water platform and a procurement center to improve operational management efficiency, reduce manpower and operating costs, and achieve value growth. At the same time, through acquiring asset-light technology companies, the company has invested heavily on research and development, including obtaining a 100% stake in Nanjing Municipal Design and Research Institute at cost of RMB 181 million in May 2014, and the acquisition of Huai`an City Water Survey & Design Institute in 2015. A number of special Grade A qualifications have been obtained to provide more technical and design services support for the company's integrated water environment management business, and to strengthen the company's comprehensive design capabilities for value chain integration. It's expected that the company's "dual platform" strategy will continue to promote each other, and the company's ability to transform from heavy assets to light assets will continue to strengthen.

Cooperation with China Three Gorges Corporation, Promising on “Yangtze River Protection”

China Yangtze Power Co., Ltd., a controlling subsidiary of China Three Gorges Corporation, subscribed for a 5% stake in BEWG through a wholly-owned subsidiary China Yangtze Power International (HK) Co., Ltd., with a total consideration of HKD 2.02 billion, of which approximately HKD 1.5 billion was spent on traditional water projects of BOT and TOT, and approximately HKD 500 million is used for a comprehensive renovation project. Yangtze Ecology and Environment Co. Ltd is a subsidiary of China Three Gorges Corporation and is positioned to undertake project implementation tasks for the Yangtze River protection-related undertakings, including coordinating the implementation of the Yangtze River Basin Hub Operation Management, implementation of major ecological restoration projects, ecological environmental management of the dam reservoir area, comprehensive environmental management, and water resources utilization projects in the basin.

In January 2019, the Ministry of Ecology and Environment and the National Development and Reform Commission jointly issued the "Action Plan for the Protection and Rehabilitation of the Yangtze River", which requires that by the end of 2020, the national control section ratio of the Yangtze River Basin with excellent water quality will reach over 85%, and the inferior V ratio will be less than 2%. The ratio of black odor elimination in the built-up areas of prefecture-level and above cities in the Yangtze River Economic Belt is over 90%, and the proportion of water quality in centralized drinking water sources at prefecture-level and above is higher than 97%. On May 29 2018, the National Development and Reform Commission held on-site meeting to promote the Yangtze River Economic Belt urban sewage treatment pilot spot in Jiujiang, indicating that China Three Gorges Corporation will lead the Yangtze River Protection.

In June 2019, the newly established joint venture company by BEWG, China Three Gorges Corporation and other companies was awarded the first PPP project in Yueyang City with a total investment of RMB 4.45 billion. The Company believes that the “Yangtze River Protection” is expected to have a market value of more than one trillion RMB, and with the company's rich experience in water treatment projects, operational advantages and sufficient technology precipitation, it can cooperate well with China Three Gorges Corporation to achieve a significant synergy effect.

Financial Forecast and Valuation

Financial Performance

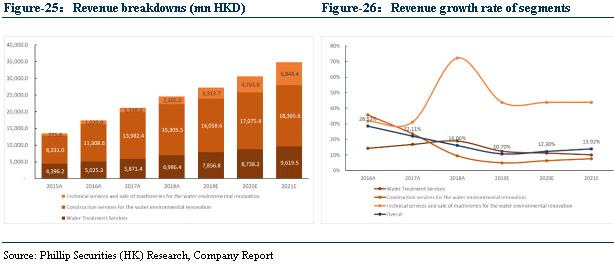

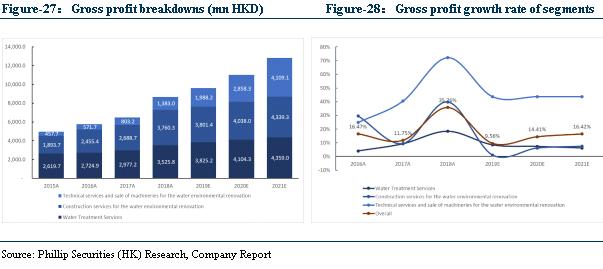

The company's revenue in 2018 was HKD 24.597 billion, representing an increase of 16.06% YoY; gross profit was HKD 8.776 billion, increasing by 35.75% YoY; gross profit margin was 35.68%, showing an increase of 5.18%; net profits attributable to shareholders was HKD 4.471 billion, increasing by 18.18% YoY. From the historical data, the company's overall revenue and gross profit maintained a relatively fast and steady growth. It's expected that as the company's light asset transformation continues, some business revenues may be affected, but the increase in gross profit margin and the light asset business will gradually raise the level of profitability for the company and bring high-quality cash flow. Through continuous mutual promotions of dual-platform strategy, the company will continue good results and profit growth.

Financial Forecast

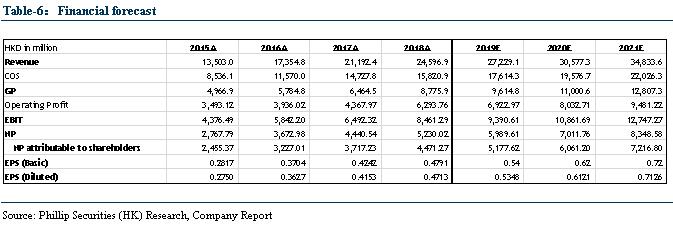

It is estimated that the company's revenue in FY19/FY20/FY21 will be HKD 27.23/30.58/34.83 billion, representing increases of 10.70%/12.30%/13.92% YoY; gross profit will be HKD 9.62/11.00/12.81 billion, representing increases of 9.56%/14.41%/16.42% YoY; net profit attributable to shareholders will be HKD 5.18/6.06/7.22 billion, representing increases of 15.80%/17.07%/19.07% YoY; corresponding EPSs are HKD 0.54/0.62/0.72. The company continued to promote the "Dual Platform" strategy and light asset transformation, and relying on the company's rich project experience and technology accumulation, it has strong alliance with China Three Gorges Corporation, complementing each other's advantages, and actively expanding the "Yangtze River Protection" trillion-yuan markets. We are optimistic about the future development of the company.

Valuation

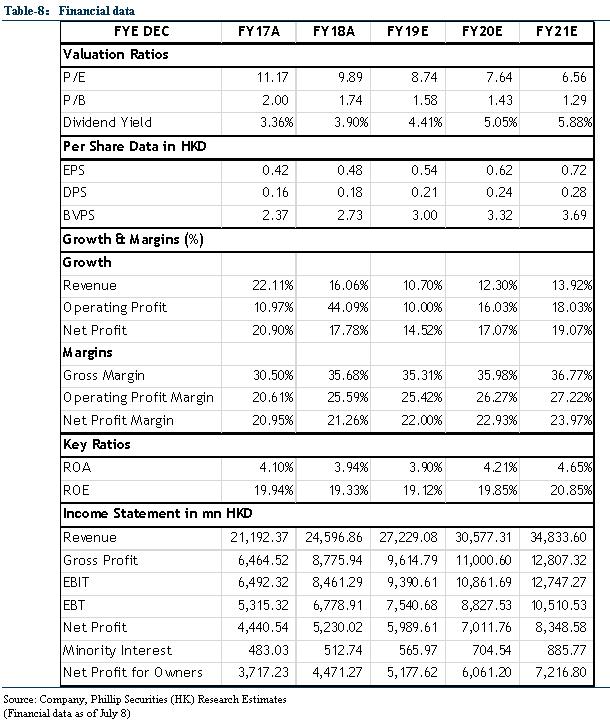

Based on our residual income valuation model, assuming the cost of equity is 9.66% and resistance factor is 0.2, we give a TP of HKD 5.81, corresponding to FY19/FY20/FY21 10.71x/9.36x/8.04x PER with a 22.57% potential upside compared with CP of HKD 4.74 as of July 8, 2019. Wind data shows that the company's expected PER of 8.96x in 2019 is attractive compared to the industry average PER 14.33x, we initiate coverage on BJ Ent Water and recommend “BUY” investment rating.

Risk

1. Industry policy risk

2. Projects development fails expectations

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()